2026 Superannuation Updates

With 30 June fast approaching, this update covers everything you need to know about meeting pension payment obligations, updated contribution caps, and key changes coming to super in the 2026/27 financial year - don't miss the important reminders and planning opportunities inside.

Pensions - Reminder to members in pension phase

If a super fund fails to physically pay sufficient pensions to meet its minimum obligations, the fund will not be entitled to the tax exemption (i.e. it will lose its tax free income status). Other than in specific circumstances, it is not acceptable for the fund to accrue any pension shortfall in its financial statements.

Importantly, pensions paid by electronic transfer need to clear the super fund bank account on or before 30 June to be considered a pension for that year.

If your SMSF is in pension phase details of the minimum pension requirements for each fund member will have been provided to you. If you have questions in relation to the minimum pension please contact our office.

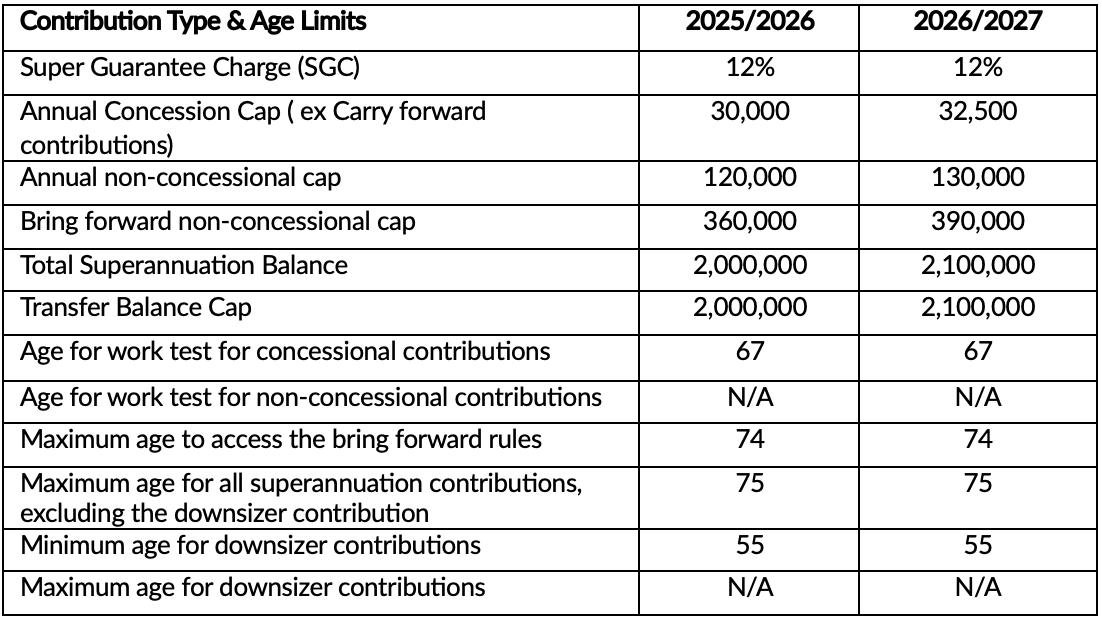

Superannuation contributions caps from 1 July 2026

From 1 July 2026, the superannuation concessional and non-concessional contribution caps will increase. The contribution caps for the 2026/2027 financial year are:

Concessional cap - $32,500

Non-Concessional cap - $130,000 or $390,000 over 3 years

The table below indicates the superannuation caps for 2026 and 2027:

If you intend to deposit funds to superannuation on a concessional or non-concessional basis it is important that they are received into the SMSF bank account on or before 30 June. Further, there are requirements to consider with respect of eligibility for such contributions which are discussed below.

Non-concessional contributions and the work test

From 1 July 2022, passing the work test has not been required for those eligible to make a non-concessional contribution to super. In addition, the bring forward 3 year non-concessional rule was extended to those up to the age of 75. Note that the work test (40 hours work in a 30 day period) is still required for those over the age of 67 who seek to make a concessional contribution to super.

The annual concessional cap and carry forward concessional contributions – what do they mean?

Historically, the annual concessional (before tax) contribution caps offered little flexibility for those who take time out of work, work part-time, or have ‘lumpy’ income and therefore have periods in which they make no or limited contributions to superannuation.

From 1 July 2019, the Government has allowed individuals with a total superannuation balance of less than $500,000 (just before the beginning of a financial year before a carry forward catch up contribution is made), to make ‘carry forward’ or ‘catch-up’ superannuation contributions. Individuals can carry forward their unused concessional cap space on a rolling basis for a period of five years. Amounts that have not been used after five years will expire.

In order to access the carry forward arrangements the current year concessional contribution cap must first be fully consumed. Any excess concessional contributions are then allocated to the oldest available unused carry fowrard balance.

As the contribution caps are a function of the individuals circumstances and not the superannuation fund, contact your accountant responsible for lodging your personal tax return to determine your modified contribution cap.

Non-concessional contributions

You can make after tax contributions to super that could come from your personal savings, transferring personal investments, an inheritance or from the sale of investments. For the 2026/2027 financial year the annual personal after tax contribution cap is increasing from $120,000 to $130,000. Further it may be possible to deposit up to 3 years of non-concessional contributions in the one financial year using the 3 Year Bring Forward Rule. This rule allows you to make substantial contributions to super and build up your retirement savings.

You are ineligible to make non-concessional contributions once you are 75 years old. However you will have 28 days after you turn 75 years for your super fund to receive a non-concessional contribution.

Important: For those individuals with a Total Superannuation Balance (TSB) aggregated over all their super funds in excess of $2M, non-concessional contributions will generally not be allowable in the FY25/26 year. In addition the 3 year bring forward provisions may be impacted if an individual’s superannuation balance is $1.76M or over. The specific workings of non-concessional contributions are technical in this regard and our office should be contacted for comment prior to considering such contributions.

From 1 July 2026 the TSB limit is being increased from $2M to $2.1M. This may allow those with superannuation balances less than $2.1M on 1 July 2026 the ability to still contribute non-concessional amounts to their super fund.

Total Superannuation Balance and Transfer Balance Cap

On 1 July 2026 The Total Superannuation Balance (TSB) and Transfer Balance Caps (TBC) will increase to $2,100,000.

The increase in the TSB will allow those with less than $2.1M in superannuation (on an individual basis) to contribute additional non-concessional contributions (as measured on 1 July in the year of making the contribution).

The increase in the TBC will allow those commencing Account Based Pensions to start these pensions with a value of $2.1M. Importantly, for those that have already commenced an account based pension with an amount less than their own individual TBC then part indexation will be available on their cap and adjusted automatically by the ATO.

Downsizer contributions – eligibility age 55

From 1 July 2018 the Coalition introduced ‘downsizing’ provisions where, in the event you sell the family home, some of the proceeds from the home sale (up to a maximum of $300k per individual or $600k for a couple) can be contributed to super. The key eligibility criteria for these provisions are as follows:

You (or your spouse) are 55 years old or over at the time you make a downsizer contribution (there is no maximum age limit).

The amount you are contributing is from the proceeds of selling your residential property where the contract of sale was exchanged on or after 1 July 2018.

The property was owned by you or your spouse for 10 years or more prior to the sale.

The proceeds (capital gain or loss) from the sale of the home are either exempt or partially exempt from capital gains tax (CGT) under the main residence exemption, or would be entitled to such an exemption if the home was a CGT rather than a pre-CGT (acquired before 20 September 1985) asset.

You make your downsizer contribution within 90 days of receiving the proceeds of sale, which is usually the date of settlement.

These contributions are bound to be popular particularly when considering:

The size of the ‘new home’ is irrelevant for the purposes of accessing the downsizer contribution.

The downsizer contribution is available irrespective of a members superannuation balance (eg individuals can still access the downsizer contributions if their super balance is in excess of $2.1M)

The property being sold does not need to be your place of residence at the time of sale – merely it must have been your place of residence at some stage during the ownership period.

These contributions will not count towards non-concessional contribution caps.

A downsizer contribution can be made after receiving a deposit for the property with a subsequent downsizer contribution allowable from the settlement proceeds, subject to the sum of the contributions being no more than the $300,000 per person limit.

Please contact our office if you have further questions with regard to the downsizer contributions.

Division 296 Superannuation Tax Update

Status:

Legislation passing the Government’s Division 296 tax, which would introduce an additional 15% tax on superannuation earnings for individuals with total super balances exceeding $3 million, has now been passed by both houses of Parliament and is now legislated. Its important to remember this tax will only apply to individuals whom have superannuation assets (excluding other personal assets) in excess of $3m.

Key takeaways:

There will be no taxing of unrealised capital gains as originally proposed.

The $3m cap will be indexed with inflation.

A new threshold of $10m (which will also be indexed) will be introduced and earnings on super balances in excess of $10m will be taxed at 40%

The commencement date is 1 July 2026, a deferral of 12 months from originally planned. This means that the first time to measure a super funds balance against the $3m threshold is 30 June 2027 with the first payment date in the FY27/28 year.

D296 tax will be based on that individuals superannuation asset earnings. The tax can be paid from either individual or superannuation sources.

Self managed super funds of all sizes will have the option of ‘opting in’ to have capital gains accrued to 30 June 2026 disregarded for the purpose of D296 legislation. We are still unsure of the mechanics of this opt-in function however it will either be part of the FY26 or FY27 tax return of the super fund.

For many it’s likely that retaining assets in super above the $3m threshold will continue to be the most appropriate course of action.

Professional guidance

We will continue to work with those impacted by the changes, noting that the commencement date has been deferred to 1 July 2026, to ensure current structures are still appropriate. Any decision to exit an asset from super to save the D296 tax needs to occur before 30 June 2027.

Important note

The information provided is general in nature and does not take into account individual objectives, financial situations, or needs. It is intended for informational purposes only and should not be relied upon as financial or professional advice. Individuals should seek tailored advice and consider relevant product disclosure documents before making any decisions.

If you have questions with regard to the proposed changes to superannuation please contact Daniel Uden to discuss.

2026 Federal Budget Changes

While there are a number of proposed changes to taxation arrangements in the recent Federal Budget none of these changes impact the superannuation environment.

A quick summary of what it means for you;

Payday Super - Superannuation Guarantee Changes

From 1 July 2026, a major change to Australia’s superannuation system takes effect. Known as Payday Super, the reform changes when employers must pay Superannuation Guarantee (SG) contributions — moving from quarterly payments to payments in line with each pay cycle.

What is changing?

Under Payday Super, employers will be required to ensure SG contributions are paid and received by the employee’s super fund within seven business days of payday.

While the SG rate remains unchanged at 12%, the timing obligation is significantly tighter and removes the flexibility many businesses currently rely on.

The minimum threshold for paying SGC was removed. This means that all employees, even those that earn less than $450 per month are eligible to receive superannuation payments from their employers.

What should you do now?

Businesses that prepare early will avoid last-minute disruption. We recommend reviewing your current payroll and super processes well ahead of 1 July 2026. Our firm will be supporting clients through this transition — from system readiness and process design through to implementation and ongoing compliance. Please contact us to discuss how Payday Super will affect your business and the steps you should be taking now.